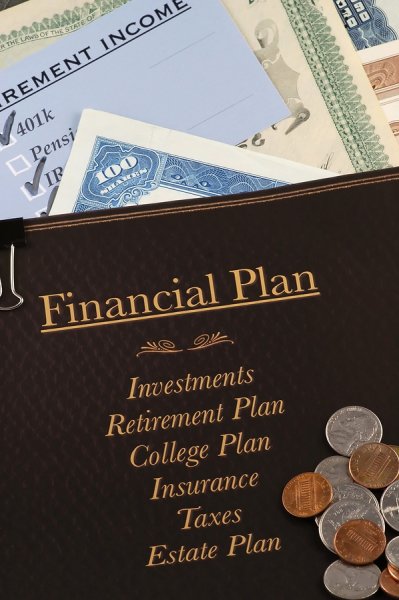

Every significant human accomplishment started with a plan. If one of your goals is to retire to a life of financial freedom, you’ll need to devise and implement a strategy by which you will guide your resources toward the accomplishment of that aim. Afterwards, reviewing your financial plan on a regular basis will help you maintain its effectiveness.

With that said, the following assumes you already have one. If you have yet to devise yours and set it into motion, now is a great time to get started.

What to Review & When

Every Month

Checking, savings and credit accounts should always be reviewed on a monthly basis. You’ll need to balance your checkbook, make sure your savings plans are proceeding the way you’d like and pay any outstanding debts — ideally before they accrue interest charges. As many Freedom Debt Relief reviews demonstrate, it’s highly important to avoid debt denial by staying on top of debts and coming up with a strategy to eliminate them.

Each Quarter

Quarterly reviews are sufficient for your retirement plans and investment accounts. Doing these monthly might be a bit too granular to return actionable data. Three months gives things time to change and enables you to stem undesirable trends before they progress too far.

This is also a good time to review your credit report. You’re entitled to one free copy of each of your reports from the big three agencies (Experian, Equifax and TransUnion) on an annual basis.

In other words, you can get three free credit reports each year. You’ll see errors before they have an entire year to grow and fester if you ask for them one at a time — on a quarterly basis.

On an Annual Basis

Look at the big picture to determine how your strategy is performing overall.

Investments: Is your asset mix still optimal for meeting your time frames and tolerance for risk, as well as your needs and preferences?

Savings: Are your savings strategies still making the most of the tax benefits available to you? Are you taking full advantage of tax-deferred accounts like 401(k)s and IRAs? In other words, are you saving tax efficiently?

Insurance: Are your insurance holdings still in line with your family’s needs? Should your beneficiaries still be the same people? Do you have a new child or grandchild? Are your children grown and gone, reducing your need for life insurance? If so, can you shift those premiums into long-term care insurance?

Estate Plan: Is your asset preservation strategy still effective? Have any of the estate and/or tax laws changed? Does your executor still know where to find everything they need to distribute your estate according to your wishes? Have there been any marriages, births or deaths that could predicate altering your estate plan?

Familial Developments: How are your parents doing? Will you need to plan to care for them within the next year or so? Are your children making it OK, will you need to give them a financial kick start? What’s your health situation like? Should you be planning for a longer time horizon than you initially estimated?

Reviewing your financial plan according to these time frames and with these questions in mind will help you protect your wealth. The other intervals aside, how you approach the annual one is purely up to you. Some people do it at the beginning of each year; others do it in the middle of the year and still others close out each 12 months seeing where they are.

However, what’s more important than when is that you do.