If you haven’t explored the world of life insurance, underwriting may seem like a confusing and deliberately mysterious process. When you fill out a life insurance application, you likely have no idea how much coverage you are eligible for or how much your monthly premium will be without some industry knowledge. That’s why we’re taking the time today to go over life insurance underwriting, how it works, and how you can make sure you are getting the best life insurance policy that will protect your family in the case of your untimely passing. With a little bit more knowledge about how insurance companies evaluate your application, you’ll feel more confident when you hit submit.

What is the Underwriting Process for Life Insurance?

Underwriting is how the insurance companies determine your eligibility and monthly cost for life insurance.

Underwriting is essentially an estimate of your life expectancy.

Underwriting is essentially an estimate of your life expectancy.

Since life insurance is designed to financially protect your loved ones after your passing, your insurance provider needs to assess the likelihood that they will need to pay out the full coverage amount before approval. To put it bluntly, the insurance company will use your application to calculate the chances that you will die during your life insurance term. This is—of course—only applicable to term life insurance policies. Whole life insurance policies also require underwriting, though they are able to guarantee a death benefit payout. This is the reason that whole life insurance policies cost more than term life insurance policies. When a provider guarantees that you will receive a large payout, you are expected to pay more for that guarantee.

In order to make a determination whether or not to provide you with insurance, the insurer will require (in most cases) that you answer a few questions on the phone, fill out an extensive medical questionnaire, undergo a medical exam including blood tests, allow access to your medical history, current prescriptions, and answer even more questions about your daily lifestyle. Using all of this information, the insurance company will place you in a risk class and will either present you with an insurance policy or a rejection letter.

Is There a Way to Speed Up the Underwriting Process?

If you need to get life insurance within a time constraint, you may want to explore getting life insurance with no medical exam

If you need life insurance quickly, you have the option to skip the medical exam.

If you need life insurance quickly, you have the option to skip the medical exam.

The application process for life insurance can deter a lot of people from exploring their options—especially the medical exam aspect of the application and underwriting process. If you are applying for a standard term life insurance policy, you’ll need to schedule the exam, undergo blood testing, and wait anywhere from 1-2 months for the results. For a lot of people, this just isn’t the best option due to the length of time required for approval & the need to get blood taken. Luckily there are ways to qualify for life insurance with no medical exam!

Getting life insurance with no medical exam is by far the easiest way to get the coverage you need as quickly and easily as possible. You will still need to provide the insurance company with some information about your life and your lifestyle habits, but you can skip the medical exam. As we mentioned, the medical exam and blood test results are the reason that underwriting takes so long to complete. So, if you are under a time constraint—or if you have a fear of needles—getting life insurance with no medical exam could be the right coverage option for you.

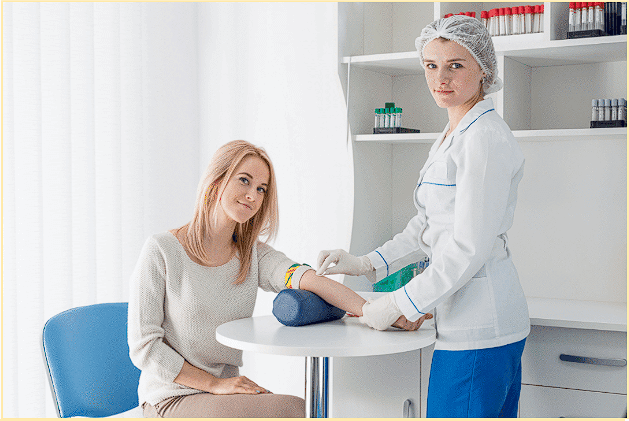

What Are the Steps For The Underwriting Process?

In order to get approved for a policy, there are a few hoops you have to jump through

The first step of the underwriting process is a lengthy application.

The first step of the underwriting process is a lengthy application.

During the underwriting process, the insurance company will get as much information from you as possible to determine your eligibility. In short, they are interested in calculating your life expectancy. In order to do this, there are several steps you will need to take in order to purchase a life insurance policy to protect your loved ones. Let’s take a detailed look at the steps you need to take to secure life insurance coverage:

- Application – For most life insurance companies, you will be asked to complete an online application where you will provide information about your health and lifestyle choices.

- Interview – Many insurance companies will want the chance to talk to you on the phone. During this phone call you can expect some more in depth questions than you were asked in the online application.

- Medical Information Bureau Verification – As part of the underwriting process, the insurance company will need access to your medical history. Even though you are asked to disclose any conditions during your initial application, the provider will still verify your information using the MIB.

- Medical Exam – As we mentioned, there are policies out there that you can get approved for with no medical exam. However, if you choose to undergo the exam you’ll need to submit to a physical and blood tests. Providers will also look for drug or tobacco use in your blood test results.

- The Results – Once all of your information is in the hands of the provider, they will assess everything they’ve gathered and decide what to offer you. If you have a chronic illness or very risky lifestyle habits, then you could either be denied coverage or you could be presented with a higher than average premium. When you are presented with the offer from the insurance company, you have the option to deny the offer and continue searching for the right policy. Should you accept the offer, you’ll enter an agreement with the insurance company and you’ll be insured!

Though the underwriting process may seem straightforward, there are a lot of different factors that will affect your ability to get approved or to get a premium that fits within your budget. That’s why in this next section we’re breaking down the aspects of your application that insurance companies will use to determine your rate.

Which Health and Lifestyle Factors Will Affect My Monthly Premiums?

You may be surprised by some of the health and lifestyle factors insurance companies assess before presenting you with an offer

Many people don’t realize that their driving record impacts their ability to get life insurance.

Now that we know the steps that are necessary for insurance companies to complete the underwriting process, we should take a moment to discuss what they are looking for. You have given the company a whole bunch of information about yourself, but what are the factors that will affect your premium or your ability to get approved? Let’s take a look!

- Health Status – If you have a chronic or life-threatening illness, you will have a more difficult time getting life insurance and there is the possibility you could be denied.

- Age – Across the industry, the older you are the more you will end up paying for life insurance.

- Driving Habits – Having a safe driving record will help you secure a lower rate. If you have a history of reckless driving you will end up paying more since you will fall into a higher risk category.

- Gender – In almost every case, men pay more for life insurance than women. This is due to men having historically shorter life expectancies than women.

- Lifestyle Habits – There are several different lifestyle habits that will affect your ability to get life insurance. For example if you are an avid skydiver, then prospective providers will take that into account before presenting you with their offer.

- Your Profession– Risky jobs like mining, logging, and commercial fishing are all considered high-risk occupations and will affect your ability to get coverage.

- Smoking Status – Since smoking has such a documented health impact, smokers pay much more for life insurance than nonsmokers.

Now that you know more about how the underwriting process works and what insurance companies are looking for, you can feel more confident submitting your application. Remember to be completely honest on your application. After all, the insurance companies have ways of verifying all of your health information. You may have read through some of the lifestyle factors and decided there are some changes you need to make before submitting your application—such as quitting smoking or a change of careers. It is also important to remember that there are policies available that can help you get coverage as quickly as possible, like no medical exam life insurance.

Overall, getting life insurance is important for protecting your family members in the future. Though the approval process may seem initially difficult, it is ultimately worth it to provide peace of mind for yourself and your family members.